Status: ✅ Approved EU law, 2025 first reporting required

The Corporate Sustainability Reporting Directive (CSRD) will standardize ESG reporting within the EU as part of the European Green Deal and the EU Textile Strategy. By requiring regular disclosures on environmental and social matters, the CSRD aims to help investors, consumers, and other stakeholders understand and compare textile companies' sustainability performance.

TL;DR

Who in the fashion industry does the CSRD affect?

Ultimately, every listed apparel and footwear company that sells into the EU market, except micro-enterprises, will be required to report under the CSRD. However, there will be a phased-in approach depending on the size of your company. The first CSRD reports will be due in January 2025, covering the 2024 financial year.

These are the different size categories that are defined in the requirements section of the Corporate Sustainability Reporting Directive:

- Textile companies that are already required to complete NFRD* reporting

- Large brands that meet two of the three criteria:

- More than 250 employees

- More than €50M turnover

- More than €25M in total assets

- Medium-sized fashion brands that meet two of the following criteria:

- Less than or equal to 250 employees

- Less than or equal to €50M turnover

- Less than or equal to €25M in total assets

- Small (listed) apparel brands that meet two of the below criteria:

- Less than or equal to 50 employees

- Less than or equal to €10M turnover

- Less than or equal to €5M in total assets

- Non-European companies with branches of subsidiaries in the EU

Note: You might see slightly different category sizes in other articles, these are outdated. In December 2023 the size criteria in relation to the impact of inflation was corrected by the European Commission. The numbers above represent the updated size criteria. Read the official documentation here.

*You may already be aware of the Non-Financial Reporting Directive (NFRD), which introduced similar reporting requirements in the EU. These were deemed insufficient, and in 2021, the CSRD replaced and expanded the NFRD's reporting requirements.

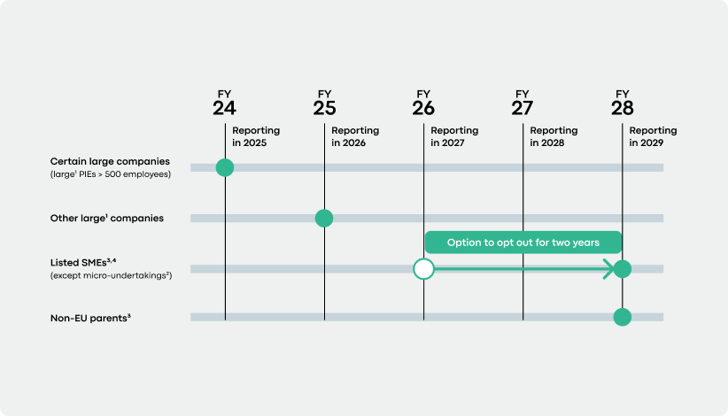

What is the CSRD reporting timeline for textile companies?

For many companies, the staggered deadline for CSRD reporting will enable them to implement carbon accounting and life cycle assessment tools and procedures in advance.

The implementation of CSRD reporting requirements will be released in four phases:

- Phase 1, 2025: European and non-European companies currently subject to the NFRD will report on the 2024 fiscal year

- Phase 2, 2026: Large brands (also and non-European if they are listed in the EU) will report on the 2025 fiscal year

- Phase 3, 2027: Listed Small and Medium Enterprises (SMEs) will report on the 2026 fiscal year

- Phase 4, 2028: Global non-EU companies with a turnover of €150 million in the EU and at least one subsidiary or branch in the EU

Tip: If you are a listed SME, you might think that 2027 is still very far in the future, but remember: you will need to report on the 2026 fiscal year. That means, you must have all your systems setup and your data available by the end of 2025. When you put it that way, 2027 isn’t that far away! Connect with the Carbonfact team to learn how we can help your textile business prepare for CSRD reporting.

What are the CSRD reporting requirements for fashion brands?

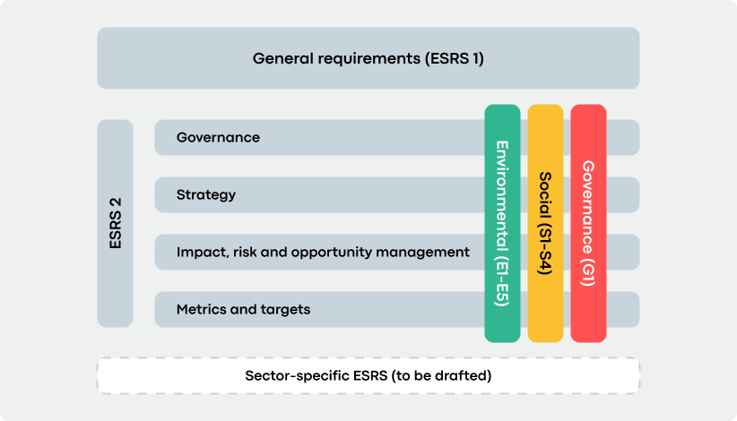

The CSRD requires textile companies to publish non-financial information in accordance with the European Sustainability Reporting Standards (ESRS) developed by EFRAG (European Financial Reporting Advisory Group).

The ESRS outlines how and what information and ESG metrics fashion brands need to report to European regulators to comply with the CSRD. Overall there are 12 European Sustainability Reporting Standards (ESRS).

In addition to the Climate Standard (ESRS E1) and the publication of Scope 1, 2, and 3 emissions information, the CSRD requires the publication of information relating to water, pollution, biodiversity, and circularity, as well as social information concerning workers and consumers.

EFRAG will also develop specific standards for the most impacting industries, including textiles. However, the textile sector-specific ESRS standards will be delayed by two years. This means that they will be published in 2026 instead of 2024. This has no implications on the CSRD reporting timelines for apparel and footwear brands.

The 12 standards can be condensed into four groups: Cross-cutting, Environment, Social, and Governance.

Cross-cutting, ESRS 1 & ESRS 2:

These standards encompass General Requirements and General Disclosures, which “cross-cut” different sectors and industries. ESRS 1 establishes general requirements, such as important concepts and principles, that must be followed when reporting under the CSRD, while ESRS 2 outlines reporting requirements that must be followed under the three topical standards (Environment, Social, and Governance).

ESRS 1 also introduces the double materiality assessment, which emphasizes the consideration of both the external impacts of an organization’s activities on the environment and society, and the internal impacts of sustainability factors on the organization's financial performance. We’ll explore this in greater detail below.

Environment (ESRS E1-E5):

These five standards require fashion companies to disclose information on greenhouse gas emissions, air and water pollution, and impacts to biodiversity. The ESRS environmental standards also dig into resource usage and circularity. Remember, this is across the entire supply chain, so you’ll need to report about everything from where materials are sourced to end-of-life for each product. Carbonfact’s sustainability reporting software helps apparel and footwear companies to measure and disclose the environmental CSRD requirements.

Read more about ESRS E.1 Climate Change below.

Social (ESRS S1-S4):

ESRS S1 to S4 represent the social indicators within the European Sustainability Reporting Standards, offering a structured approach for textile brands to report on their social and human rights performance. These provide information on social matters, including employee-related aspects, human rights, and diversity policies. This includes company employees as well as workers across the value chain.

Governance (ESRS G1):

The governance standard emphasizes corporate governance, including structures, processes, and policies that influence decision-making within an organization. It encourages transparency and accountability in disclosing information related to governance structures, the composition of boards, and measures taken to ensure ethical and responsible business practices. Companies will be asked to describe their business model and how sustainability considerations are integrated into their strategy. They are also required to report on how the company identifies and manages sustainability-related risks.

ESRS E1 Climate Change

Among the 12 ESRS reporting standards, the ESRS E1 standard on climate change is the most detailed and demanding. It includes nine disclosure requirements and is one of the most comprehensive standards.

- Fashion companies must share their absolute emissions in Scope 1, 2, and 3 (absolute value and intensity)

- Determine if a transition plan is in place that is aligned with the Paris Agreement.

- Analyze the impact of all your activities on the climate.

- Estimate the current and future impact of climate change on your organization's operations.

- Provide details on all internal initiatives taken to reduce or mitigate the negative impact on the climate.

- Establish reduction targets that are consistent with the objectives of the Paris Agreement.

- Develop an action plan that outlines how to achieve these objectives.

There is in the ESRS E1 a clear reference to GHG protocol as one of the methods that can be used.

There is in the ESRS E1 a clear reference to GHG protocol as one of the methods that can be used.

Carbonfact's approach

Carbonfact is a CSRD reporting software built for the needs of the fashion industry. We help you:

- Centralize all the primary and secondary data that you need for the environmental reporting standard

- Calculate all the required Scope 1, 2 and 3 emissions and

- Automatically transform the data into the CSRD reporting format, so you just need to hit export.

Double materiality

This is a new reporting requirement presented by the CSRD. Simply explained, for each of the ten topical standards in the ESRS, textile companies will need to conduct a materiality assessment, determining what data points are relevant (i.e., “material). If not relevant—or material—companies will not be required to report on them.

It assesses how business actions affect or may affect both sustainability and financial aspects. Taking ESRS E1 Climate Change as an example, what is the impact of climate change on their business financially, and what is the business’s impact on climate change.

That said, for apparel and footwear brands, many of the standards, such as Climate Change, Labour Rights, etc, will definitely be material.

Other CSRD requirements relevant to textile companies

- Targets: The Corporate Sustainability Reporting Directive mandates textile organizations to establish concrete targets, choose a baseline, and report their progress in achieving these specified objectives.

- Audit requirement: The CSRD introduces an audit assurance requirement for its reporting. This begins with limited assurance in 2026, followed by reasonable assurance two years later. While this is a rigorous undertaking for many companies, the end result will help curb greenwashing and ensure ESG reporting meets the same standards as financial reporting.

How can you prepare now for CSRD textile reporting requirements?

CSRD reporting deadlines are around the corner, with hundreds of brands already obligated to submit reports on the 2024 fiscal year. It’s essential that fashion and textile brands of all sizes start preparing now.

We recommend:

-

Conducting a double materiality assessment. As mentioned above, double materiality is a new reporting requirement. The first step in a materiality assessment is identifying what data points are considered “material” and will need to be reported on.

-

Conducting a data gaps analysis: Find out what primary data you already measure, where it is located, and what you haven’t yet measured.

-

Select the right CSRD reporting software: You will need to select the right tools that will help you centralize, provide, and analyze all the data points that you are required to report on. For the environmental standards, for example, you will need the following features:

-

- Carbon Accounting on Scope 1, 2 and 3 emissions

- Product life cycle assessment to calculate product emissions and energy usage

- Scenario simulation tools to build concrete transition plans and measure your progress

- Reporting tools to transform the data into a CSRD-compliant format

As mentioned above, even if your company’s reporting deadline isn’t until 2026 or 2027, you will need to begin tracking this data within the next two years.

Omnibus Simplification Package and its Impact on CSRD

Introduced on February 26, 2025, the Omnibus Simplification Package proposes key changes to CSRD, CSDDD, and the EU Taxonomy, aiming to simplify compliance requirements. However, it has sparked debate, as reducing the number of companies required to report could weaken transparency and limit industry-wide sustainability data.

Key proposed changes to CSRD:

- Reduction in the Scope of Reporting Companies: The CSRD reporting threshold will increase to companies with more than 1,000 employees. This change removes approximately 80% of companies currently within the CSRD’s scope, aligning it more closely with CSDDD thresholds. Listed SMEs will no longer be required to report under CSRD.

- Postponement of Reporting Deadlines: The reporting start date for Wave 2 and 3 companies is postponed by two years.

- Value Chain Data Limitations: For companies with fewer than 1,000 employees, reporting will be voluntary under a simplified standard based on VSME ESRS (Voluntary SME Standard). Brands within CSRD’s scope cannot demand additional sustainability data from their smaller value chain partners beyond this voluntary standard.

- Revision of European Sustainability Reporting Standards (ESRS): Reduce the number of required data points, making reporting simpler. Clarify unclear provisions and improve consistency with other EU regulations.

- Removal of Sector-Specific Standards: The requirement for sector-specific sustainability standards is eliminated, reducing compliance complexity.

-

Assurance Requirements Adjustment: The proposal removes the transition to reasonable assurance, keeping limited assurance as the only requirement.

.png?width=2000&height=738&name=23138%20(1).png)

However, the Omnibus is still in the proposal stage and must go through the legislative process before becoming law. If it is not enacted by December 2025, Wave 2 companies will still need to report in 2026.

With this uncertainty, apparel and footwear brands should continue preparing for compliance to avoid last-minute challenges. Carbonfact can help navigate these changes with data-driven solutions for CSRD reporting, ensuring your sustainability strategy remains robust — regardless of shifting timelines.

Read all about the Omnibus Simplification Package here,

Prepare for CSRD with Carbonfact

Carbonfact is a CSRD Reporting Software tailored to the needs of fashion and textile brands. Our solution helps brands and suppliers track, measure, and report in accordance with the ESRS, ensuring they can accurately report on the CSRD. Because our team specializes in the fashion and textile industries, we are uniquely positioned to help companies navigate new EU and U.S. regulations around environmental sustainability.

Not only does Carbonfact help apparel companies stay compliant and report their environmental footprint, but we also minimize your manual effort with our intelligent tools, such as automated data collection, “smart filling” to overcome data gaps, and real-time life cycle assessments to understand and respond to current challenges.

Resources and further reading

- For an overview of all European textile regulations read this article and check out our textile regulations hub.

- Official website from EFRAG

CSRD crash course for textile brands

![[Guide] Carbon accounting for fashion, textile, apparel, and footwear companies](https://www.carbonfact.com/hs-fs/hubfs/CA%20-%20Opt1.png?width=600&name=CA%20-%20Opt1.png)

Angie Wu

Angie Wu

Lidia Lüttin

Lidia Lüttin